Asia Pacific leads digital currency explorations

The Asia Pacific region leads in exploring central bank digital currencies but stays cautious on implementation

The Asia Pacific region is at the forefront of exploring central bank digital currencies (CBDCs), and it’s not just driven by China and the more advanced nations. Interest is also rapidly rising in the region’s emerging economies and low-income nations.

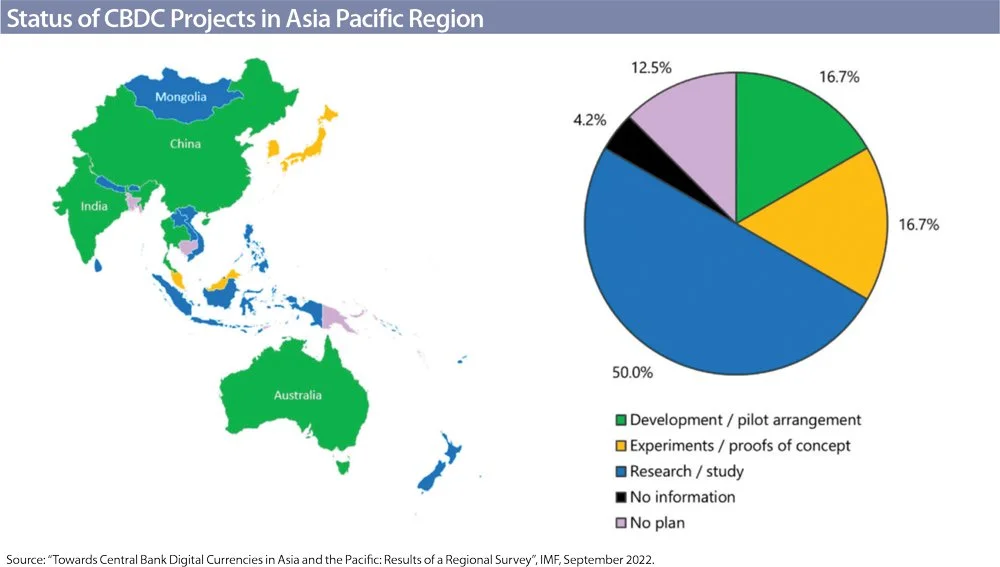

The International Monetary Fund said four of the 25 Asia Pacific economies it surveyed earlier this year are at the stage of piloting an advanced development of CBDCs. Another five are at proofs-of-concept and experiment stage and 12 are conducting research, the IMF said in a report on the survey findings published in September. The progress is ahead of other regions.

China is clearly the first mover, not just in the region but also among major economies globally. It has been researching CBDCs since 2014 and piloting its e-CNY digital currency since December 2019. The currency is currently on trial use in 23 cities and areas across the nation with over 260 million e-wallets opened. As of August 31, 2022, transactions using e-CNY had surpassed the 100 billion RMB (US$13.9 billion) mark, a figure that is still a negligible fraction of China’s total money supply. A technical test of the cross-border use of e-CNY is also under way in Hong Kong.

Meanwhile, emerging markets such as India and Thailand are at advanced stages of development, with plans to launch pilot schemes in the near term.

Australia announced a limited scale CBDC pilot in August. Hong Kong, South Korea, Japan, Malaysia and Singapore have started experiments or proofs-of-concept. A number of low-income countries, including Nepal, Bangladesh and Maldives, are studying CBDCs.

As of September 2022, 11 countries have formally launched digital currencies, according to the CBDC Tracker compiled by Atlantic Council, a US policy think-tank. They are the Bahamas (Sand Dollar), eight Eastern Caribbean nations (DCash), Nigeria (e-Naira) and Jamaica (JAM-DEX).

In addition, 105 countries representing more than 95% of global GDP are exploring CBDCs in some form. That’s a big jump from only 35 countries that were considering the concept in May 2020.

CBDCs and cryptos

In Asia Pacific, interest in CBDCs is intertwined with the development of crypto assets, which went through a phenomenal boom before the recent bust.

While it’s not surprising for advanced Asia Pacific economies such as Australia, Hong Kong, South Korea and Singapore to have large volumes of crypto transactions, even nations such as Mongolia, the Philippines, Thailand and Vietnam saw transactions amounting to more than 20% of their gross domestic product in 2021. The surge in crypto assets has accelerated central banks’ interest in digital currencies as a potential tool to safeguard their monetary sovereignty and payment systems.

The crypto sell-off which started late last year and the ensuing “crypto winter” in 2022 have had a significant impact on Asia. The failure of the crypto asset Luna and its associated algorithmic stablecoin TerraUSD, which were administered by Seoul-based Terraform Labs, has prompted South Korea and other countries to tighten regulatory scrutiny. This has further strengthened policymakers’ interest in CBDCs, with the added motivation of protecting consumers.

According to the IMF report, the key reasons for high income countries in Asia Pacific such as Australia, Japan, South Korea and Singapore to pursue CBDCs are the currencies’ ability to enhance the efficiency and safety of the payment system, lower transaction costs, and to satisfy growing demand for digital payments.

Promotion of financial inclusion and financial stability are additional motivations, especially for middle-income countries such as Malaysia, the Philippines and Thailand, while regional development is a key driver for low-income countries such as Laos and Nepal. For India, an important consideration is to maintain monetary sovereignty.

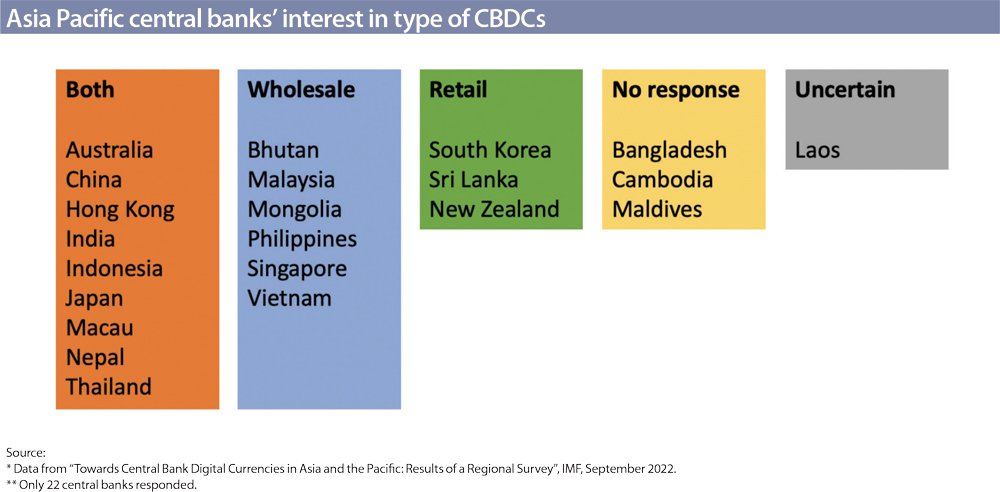

Retail and wholesale

Nations are exploring both retail and wholesale CBDCs.

Interest in retail CBDCs stems from the desire to meet demand for digital cash or digital payments and provide an alternative to private crypto assets. Asia Pacific central banks are increasingly concerned about the potential risks of cryptocurrencies on financial stability, and their impact on the effectiveness of monetary policy. This is particularly the case in developing economies.

Thailand, for example, banned cryptocurrencies as a means of payment in April 2022 out of concerns surrounding the risk of currency substitution and weakening of monetary policy. Indonesia and Vietnam have also disallowed the use of cryptocurrencies for payments. China has banned all crypto transactions and activities.

Singapore has been wooing crypto players to develop the city state as a crypto hub. But it banned all crypto advertising in public areas in February 2022 to prevent retail speculation and risks to society.

Japan is an exception in letting crypto assets be connected to the existing payment system through registered crypto asset exchanges. This allows the exchanges to receive bitcoin from users on the blockchain network and transfer the corresponding fiat currencies through existing payment systems.

The motivation for developing wholesale CBDCs focuses on enhancing payment system efficiency and security, particularly for cross-border transactions, while reducing transaction costs.

For example, Project Dunbar by the central banks of Australia, Malaysia, Singapore and South Africa together with the Basel-based Bank for International Settlements jointly explores the use of CBDCs for international settlements. Early results from the multiple CBDC mBridge Project involving China, Hong Kong, Thailand and the United Arab Emirates in collaboration with the BIS showing promising results in terms of saving time and cost.

These regional initiatives aim to solve interoperability challenges between nationally issued CBDCs and multi-CBDC platforms.

The operational model of the Asia Pacific CBDCs hinges on country-specific characteristics.

Generally, there is a preference for a hybrid or two-tier CBDC architecture where the central bank is the issuer and the private sector is the distributor. This would allow for leveraging the professional experience and advantages of authorised operators to keep technology up to date and avoiding concentration of systemic operational risk. A combination of centralised and distributed ledger design is used to enhance the resilience and expansibility of the system.

Australia, China, Japan, South Korea, and Thailand have all opted for such designs.

Features

There is a preference for CBDCs to be non-interest bearing with limits on individual holdings so as to prevent potential financial instability. These design choices are intended to reduce competition between CBDCs and bank deposits and prevent the risk of runs on banks during financial stresses.

There is also an emphasis on interoperability with existing payment networks as well as with other CBDCs and open source blockchain networks.

For example, the ongoing e-CNY technical test in Hong Kong aims to achieve interoperability with the city’s Faster Payment System connecting banks and digital wallet operators. Thailand’s retail CBDC is intended to be interoperable with the existing payment system through bridge or application programming interface gateways.

China’s central bank has clearly defined three general principles for cross-border use of CBDCs, focusing on interoperability between different CBDC systems as well as between the currencies and traditional payment systems.

Challenges

In spite of the progress thus far, the IMF survey found that all countries are grappling with a multitude of challenges. There are nine main areas: privacy, interoperability, performance and scalability, cybersecurity, compliance, legal framework, implications on monetary policy and financial stability, operational robustness and resilience, and technology-enabled functional capabilities.

Solutions are still being tested through pilots. For example, the Hong Kong Monetary Authority recently launched its third CBDC project, Sela, jointly with the Bank of Israel and BIS to delve into cybersecurity issues in the context of retail CBDCs.

Despite the shared sense in Asia Pacific that CBDCs may bring significant benefits for many economies, only China and India responded in the IMF survey that they are very likely to issue a retail CBDC in the near term.

Australia, Hong Kong, Japan, South Korea and Singapore have undertaken comprehensive research and development efforts to be technically ready but do not foresee any immediate need to issue CBDCs. And no economy in the region is committed to issuing a wholesale CBDC in the near to medium term.

“The identification of use cases, along with complex design and policy issues, requires careful consideration at the country level,” the IMF report says.

Policymakers in Asia Pacific are likely to take a cautious approach to implementing CBDCs through incremental upgrades rather than a total overhaul of existing systems.

*This article was published by Asia Asset Management’s November 2022 magazine titled “Forging ahead”.