ESG funds ready for take off in China

China’s blueprint for national development is pushing ESG into the mainstream

Sustainability is now the hottest theme in global capital markets. Pressing concerns about climate change and the coronavirus pandemic have built a powerful narrative around environmental, social and governance investing. Sales of ESG funds have reached record levels.

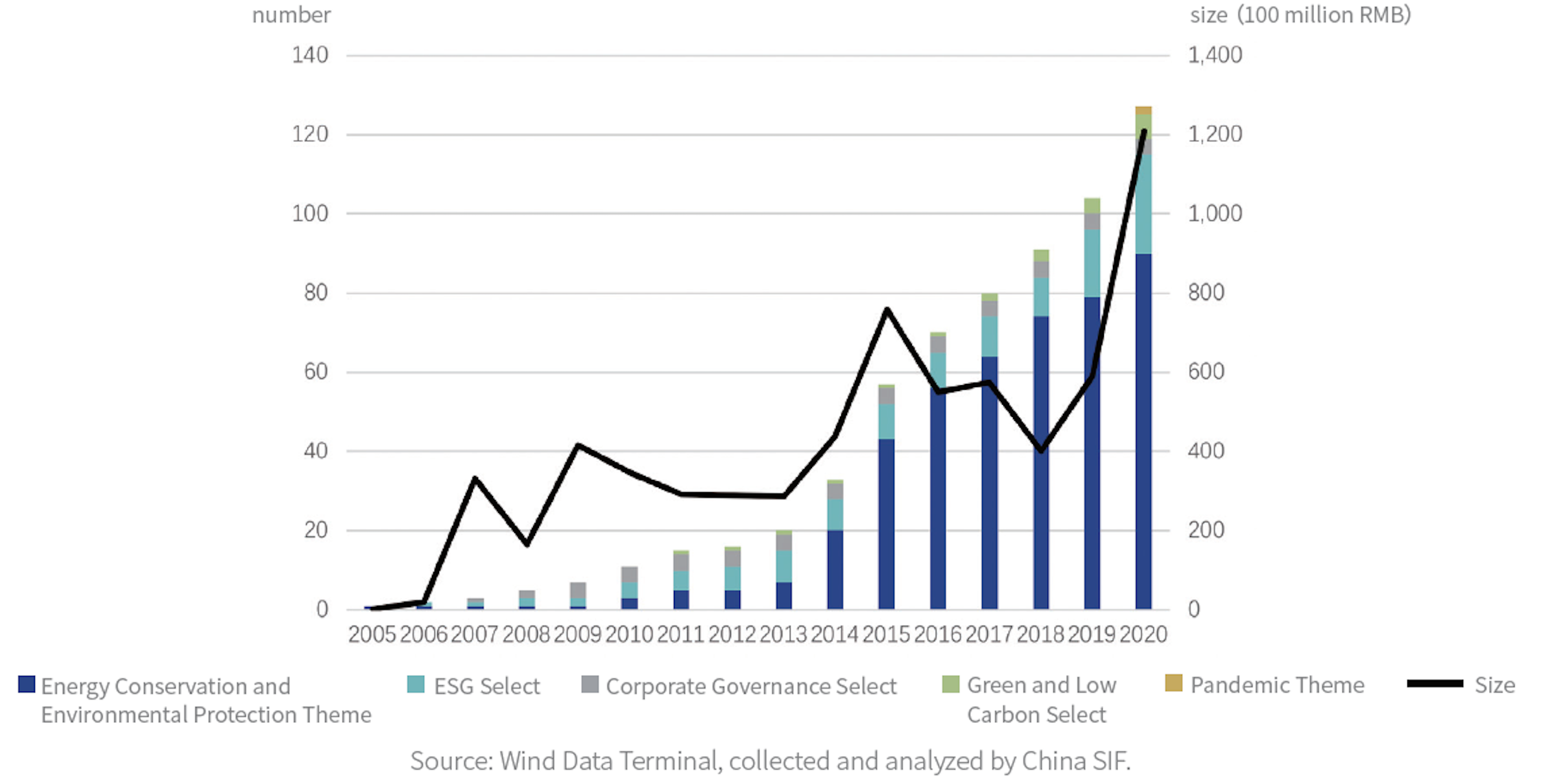

Although China is a late starter to the game, it has seen a significant uptake of ESG funds over the past two years. As of July 15, there were 164 ESG-related public investment funds with total assets of over 160 billion RMB (US$24.8 billion), according to financial data provider Wind Information. A majority of them are active or ETF equity funds. Assets have more than tripled from 2018, when China A-shares were included in the MSCI Global Emerging Markets Index. There were just 83 ESG funds in the market then.

Among the 164 funds now, 18 are labelled as ESG funds and the rest are labelled as clean energy, environmental protection, low-carbon economy and the like. Thus far this year, 33 new ESG-related funds have been launched and at least another 15 are under preparation.

Meanwhile, the number of ESG-linked stock indices tracking China A-shares has risen to 52 in 2020. And over 1,000, or 27% of listed companies in China, issued ESG reports in 2020, more than double from 2010, including 86% of the largest 300 companies by market value, though there is much room for improvement in the quality of reporting.

In addition, there are 67 ESG-linked bank wealth management products in the market, a majority of them fixed-income investments. These products have more than 33 billion RMB of total assets, according to estimates by the China Social Investment Forum.

Growth of China ESG-linked mutual funds (2005-2020)

The evolution

ESG investing in Western countries evolved from socially responsible investing, which has been around for several decades. As investors became increasingly concerned about risks from climate change and environmental issues, and the benefits of responsible business conduct, demand for aligning investing with sustainability values started to gain traction in the mid-2000s.

ESG issues were first described in a 2006 report by the United Nations-supported Principles for Responsible Investment. ESG factors eventually began to be incorporated into investment processes, moving away from short-term perspectives of risks and returns.

Meanwhile, more and more industry and academic studies suggest that ESG investing can help improve risk management and produce returns that are superior to traditional financial investments in the long term. The trend has gained strong support from regulators, and ESG assessments are embedded into listed companies’ disclosure responsibilities, adding to the momentum.

ESG investing in China has been largely led by policy and regulation rather than being investor or market driven. Similar to Western countries, it evolved from the concept of corporate social responsibility or CSR. The Shenzhen Stock Exchange issued guidelines for CSR in 2006 and the Shanghai Stock Exchange followed suit two years later, setting the stage for the Industrial Bank to launch China’s first public fund with an express focus on socially responsible investing in November 2008. The fund raised 885 million RMB in its initial offering.

Meanwhile, in Hong Kong, the stock exchange enhanced its guidelines on ESG in December 2015, requiring listed companies to make disclosures on three environmental and eight social indicators in their annual reports. As a result, Chinese companies listed in Hong Kong began making ESG disclosures even before Mainland bourses also made it compulsory in 2018.

In 2016, the People’s Bank of China (PBOC) and several government bodies issued guidelines on establishing a green financial system, which promoted investment in a wide range of assets including clean energy projects, green transportation and green buildings.

The inclusion of A-shares in the MSCI benchmark in 2018 marked a watershed for ESG development in China. Regulators and stock exchanges issued a series of new and enhanced regulations to meet the expectations of international investors on ESG disclosure and assessment. The following two years saw strong inflows into ESG funds, boosting total assets by more than 150% to 127 billion RMB as of end-2020.

In September 2020, Chinese President Xi Jinping said in his speech to the United Nations General Assembly that China aimed to become carbon neutral by 2060 and have greenhouse gas emissions peak by 2030. These goals were incorporated into the country’s five-year plan covering 2021-2025 and its 2035 vision as the blueprint for development, accelerating sustainable investments and pushing ESG into the mainstream.

Sustainable investment is a key component of China’s strategy for a green financial industry. PBOC, China’s central bank, estimated in 2015 that at least 2 trillion RMB per year would be required to invest in green sectors in order to meet the environmental targets, and that public finance could only provide 15% of the funding required. Hence, private capital, whether onshore or foreign, will be critical.

Thus far, financing has been done largely through green loans and green bonds supported by institutional investors. China’s outstanding green loans were about 12 trillion RMB at the end of 2020, putting the country in the top spot globally. Outstanding green bonds were about 800 billion RMB , the second largest in the world after the US. Onshore investors took up 72% of these bonds.

Retail market

But China’s retail investment market has been largely untapped. Despite their recent speedy growth, ESG-related funds currently account for less than 1% of the 2.3 trillion RMB domestic mutual funds market. China also accounts for less than 1% of the $1.98 trillion global ESG funds market which is dominated by Europe with an 83% share, while the US has a 12% share. China has a long way to go in luring individual investors into ESG funds.

ESG adoption by China’s mutual fund industry is progressing slowly. As of end-June, 15 of the country’s 150 mutual fund companies had signed up to the UN-backed Principles for Responsible Investment.

This February, the Asset Management Association of China released results of a survey that asked its members for a self-assessment on their green investing practices. It found that only 40% of retail fund companies sampled reported that green investing had been incorporated into their strategic planning. Furthermore, just one-third of the group had set up green investing targets and only 38.5% disclosed whether they had fulfilled their internal goals. The slow progress in ESG adoption was further complicated by a lack of uniform evaluation standards and tools and a dearth of high quality and reliable ESG data.

This is also echoed by a survey of 3,019 individual investors on their attitudes towards ESG investing conducted by China SIF and Sina.com last October. That poll found that 89% of respondents have no understanding of sustainable investment and 42% have never even heard of terms such as green finance, sustainable investment or ESG, although many of them claimed they would subconsciously factor in environment, health and business ethics in their investment decisions.

This implies that Chinese retail investors generally look at ESG funds as a new theme designed for tapping potential opportunities under the national agenda, not necessarily as a culture and belief driving the investment process. Case in point: clean energy funds account for 70% of total assets of the 33 new funds launched thus far this year.

There is nothing wrong with this as the primary motive for investing. But fund managers need to bear in mind that performance will be the key driver for asset growth at this point, unlike the more multi-faceted drivers seen in the West.

The current global taxonomy for ESG standards and frameworks has been developed primarily by the European Union and the US given their longer history in ESG adoption and their much larger ESG asset pools. But this is a problem for China, which does not regard the taxonomy as being entirely suitable to address its specific social and economic development issues.

China is developing its own taxonomy based on modified standards and frameworks with different priorities, metrics, timelines and rating systems. In the meantime, it’s working with the EU on a common green taxonomy.

Fund managers looking to replicate ESG strategies from overseas markets can be left disappointed that they may not work in China. The most critical success factor will be aligning the strategies to the government’s agenda.

Investor interest and increasing momentum on ESG adoption by Chinese companies and fund managers are forming the building blocks for ESG funds to take off in the country. But China’s ESG journey will be on its own terms, based on its own needs and characteristics.

*This article was published in Asia Asset Management’s August 2021 magazine titled “Ready to take off”.