Moving to T+1 settlement

A shorter trade settlement cycle helps to cut risk in volatile markets

A major infrastructure change is set to be implemented in the next two years which will have a profound impact on global financial markets.

A financial market industry steering committee in the US, under the leadership of the Securities Industry and Financial Markets Association, the Investment Company Institute (ICI), and The Depository Trust & Clearing Corporation, which collectively represents brokers, mutual funds, and banks, has initiated an industry change to accelerate the settlement cycle from trade date plus two days (T+2) to trade date plus one day (T+1).

Last December, the committee published a report which summarises potential issues identified by various industry working groups, and presents recommendations for the industry to accelerate the settlement cycle to T+1. The initiative is supported by the Securities and Exchange Commission.

The industry has arrived at a consensus that T+1 is the optimal next step for shortening the US equities markets’ settlement cycle. The committee recommends migration to T+1 in the first half of 2024. The report lays out a two-year roadmap for market participants to assess changes required at the firm level and allocate resources and budgets accordingly to support the migration, including the creation of a comprehensive testing plan in 2023.

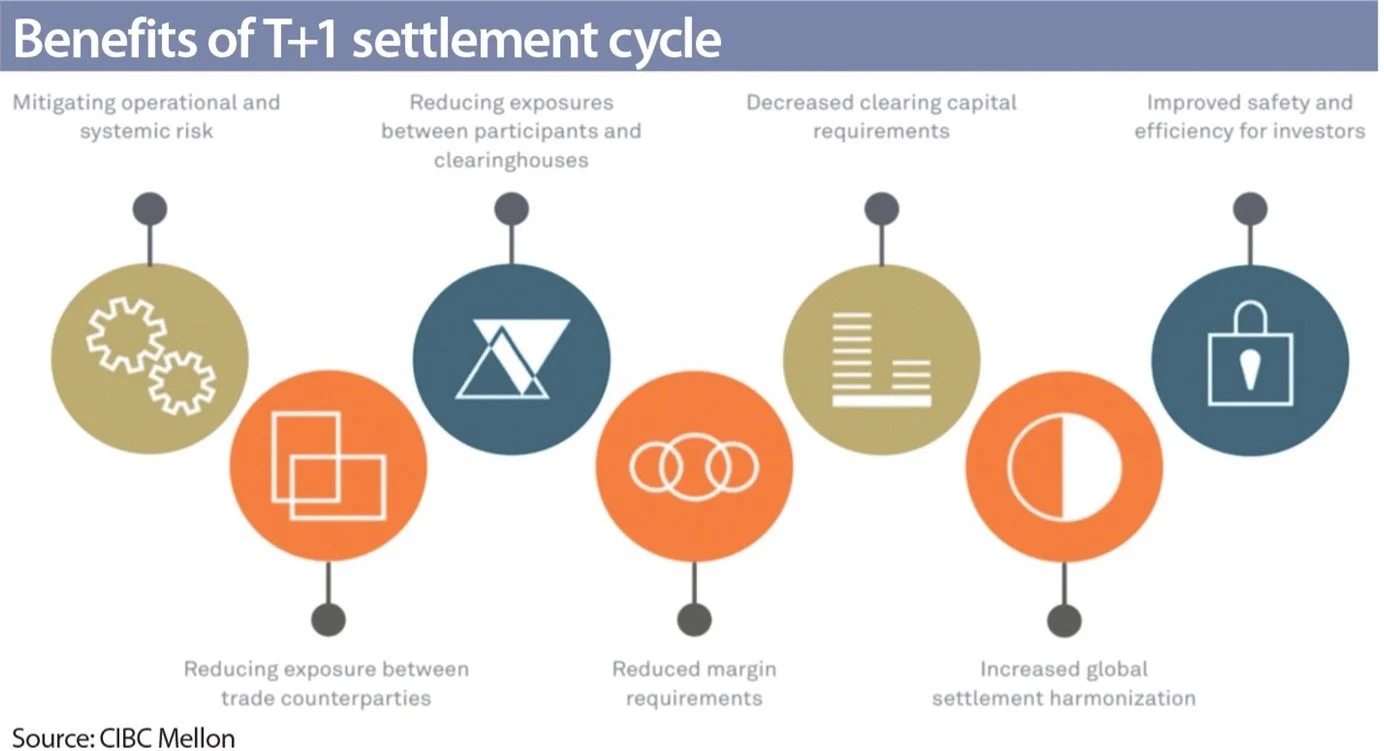

The length of the settlement cycle is very important to financial markets because of the risk that a counterparty to a trade may not fulfill its obligations between the time a trade is executed and when the securities settle. The longer the time, the greater the risk.

The risk becomes elevated during times of high volatility and stressed market conditions, such as during unpredictable events, which can potentially impact the transfer of cash or ownership of securities.

There is no standard timeframe for the settlement cycle across different markets. In the early days of their development, securities were in physical certificate form. Payment by the buyer was only made upon receiving the certificates from the seller. Delivery between cities could take weeks by horse, or months by sea voyage between countries. With the creation of stock exchanges and central counterparty clearing houses, settlement periods were gradually shortened to between five and 14 days.

But with long settlement cycles, prices could fluctuate significantly between the trade date and the settlement date. Multiple trades could also have taken place at the back of the initial trade before it was ultimately settled. If a counterparty defaults during the process, it would create a domino effect impacting the participants and the market.

After the Black Monday stock market crash in the US on October 19, 1987, stock markets across the world agreed to compress their settlement periods to T+3 by accelerating computerisation of processes and securities dematerialisation.

US securities markets operated on a T+3 settlement cycle for more than two decades after switching from T+5 in June 1995. In September 2017, they moved to T+2, which had long been the norm in many European Union countries and leading markets in the Asia Pacific region such as Australia, India, Indonesia, Japan, Hong Kong, Korea, New Zealand, Singapore and Taiwan.

The success of that transition has boosted the confidence of the US financial industry to further reduce the settlement cycle by taking a full day of risk out of the markets in the wake of increasingly unprecedented transaction volumes and volatility.

Canada has followed the US lead, announcing this January its plan to transition to T+1 for implementation in the first half of 2024. The move by the two North American markets is sure to result in a wave of T+1 implementation across EU and Asia Pacific markets, which have been vanguards in adopting shorter settlement cycles and would not want to be seen as falling behind.

Lower margin requirements

Shortening the settlement cycle will also reduce margin requirements for market participants.

Currently, counterparty clearing houses worldwide mitigate counterparty risk for centrally cleared activities by guaranteeing settlement of all cleared trades. However, since a longer settlement cycle equates to increased risk, market participants face higher margin requirements with a two-day settlement cycle to manage those risks.

A reduction in margin requirements will translate into improved liquidity and pricing to the end investor. The Depository Trust & Clearing Corporation estimated that a shift to T+1 could result in a 41% reduction in the volatility component of the clearing house’s margin requirements.

The need for a shorter settlement cycle was highlighted early last year when online trading app Robinhood, along with other trading platforms, temporarily shut down the purchase of popular meme stocks such as GameStop and GME as it scrambled to meet billions of dollars in margin requirements. The margin requirements would have been smaller if the settlement process were faster. Investors felt like they were being robbed of potential gains and the incident prompted online outrage, sparked lawsuits, and led to congressional hearings where many industry players pleaded for a shortening of the settlement cycle.

With all these clearly identified benefits, it begs the question as to why the US markets do not accelerate the settlement cycle straight to same day, or T+0.

“T+0 is not achievable in the short term given the current state of settlement ecosystem. A move towards a shortening of the settlement cycle to T+0 would require an overall modernisation of current-day clearance and settlement infrastructure, changes to business models, revisions to industry-wide regulatory frameworks, and the potential implementation of real-time currency movements to facilitate such a change,” the US report says.

But the transition from T+2 to T+1 will be significantly more complex than the move from T+3 to T+2. With the sharply compressed window, all post-trade processes will have to be done by the trade date. It will put a lot of pressure on operations, and potentially cause an increase in failed trades. It will require a rethinking of all the processes in trade execution, processing, financing, payments, and settlements.

Moreover, the foreign exchange market still largely works on a T+2 settlement cycle, which means that a one-day disconnect will exist between a securities trade and its currency exchange component. This will have to change, otherwise the operational complexity and costs will increase.

There are also other issues with regard to prime brokerage, securities lending, creation and redemption of exchange-traded funds, equity and debt offerings, and regulatory impacts to be resolved.

India gets a head start

This February, India, which had operated on a T+2 settlement cycle for 19 years, became only the second equity market in the Asia Pacific region after China to transition to T+1. China’s equity markets have been operating on a T+1 settlement cycle since they re-opened three decades ago.

India operated on a T+14 settlement cycle during the 1990s. It then shortened the cycle to T+5 in 2000, followed by T+3 in 2002, and then T+2 in 2003.

The Securities and Exchange Board of India (SEBI) first mooted the idea of shortening the cycle by one more day back in 2002 but it did not gain momentum. The subject was revived over the past five years, and this time there was popular support among local market participants. Moreover, recent improvements to India’s payment and settlement systems have enabled over 90% of payments and deliveries to the counterparty clearing houses already practically being completed by T+1.

The proposal initially raised concerns from the Asia Securities Industry and Financial Markets Association and the Association of Global Custodians that it would create operational complexities for US and European foreign portfolio investors (FPI) operating in different time zones without a trading desk in Asia. These FPIs account for around 60% of foreign investment in India.

“FPIs would have to predict the entry price and pre-fund (early pay-in) for their transactions. Further, since they invest in India from different time zones, it could also be a challenge for them to obtain permissions for stock transfers and other procedures from their respective custodians or head offices,” Akshay Thakurdesai, head of BNP Paribas Securities Services in India, says in response to questions from Asia Asset Management.

BSE, formerly Bombay Stock Exchange, and the National Stock Exchange of India, with the endorsement of SEBI, announced last November the introduction of T+1 settlement in phases starting in February 25 this year, first with the bottom 100 stocks by daily market capitalisation averaged in October. The next lowest 500 stocks would be added on the last Friday of each month beginning in March, and the final batch of more than 5,200 stocks by January 27, 2023.

Since FPIs largely trade the top 500 stocks, they will have until September/October this year to get ready for the changes. “This will help smoothen the migration process for FPIs as well as their service providers,” Thakurdesai says.

India’s stock markets have been growing steadily over the past five years, fuelled by buzzing initial public offering activities, record low interest rates, and massive growth in retail investments. The Morningstar India Index rose 30% in 2021 to a new record high, and averaged 16.3% growth per year over the last five years. This March, India overtook the UK to become the fifth largest market in the world by equity market capitalisation.

There have been several instances in the past when a buyer did not get shares due to short selling by the seller. On the other hand, the trading brokers failed to pay funds held by their clients, as technically the brokers have to pay stock exchanges on T+1. “A shorter settlement cycle helps in limiting the systemic risk by reducing counterparties’ exposures to each other,” Thakurdesai says.

India’s transition to T+1 settlement will be keenly watched by other markets. It provides an opportunity for the financial industry to modernise their trading and settlement infrastructure, and for custodians, brokers, and other players to innovate solutions for clients by guiding them through the nuances of the Indian markets and regulations. This will make the Indian capital markets more attractive to both local and foreign investors in the long run.

*This article was published in Asia Asset Management’s May 2022 magazine titled “Moving to T+1”.