Competition in China’s custody market stiffens

China’s custodian banks have been on a roll over the past two decades. But now their margins are being squeezed and new challengers are appearing on multiple fronts.

The custody industry in China started on the back of a regulation introduced by the State Council in November 1997 that required investment management to be segregated from custody of funds’ assets.

Three months later, the Big Five – Agricultural Bank of China, Bank of China, Bank of Communications, China Construction Bank, and Industrial and Commercial Bank of China (ICBC) – were granted licences as custodians to the first batch of closed-end funds launched in 1998. At the end of that year, the five banks had 10 billion RMB (US$1.57 billion) of total assets under custody (AUC) – and that was the sum total of the market.

Then came the introduction of open-ended funds in 2001. With that, the fund management industry took off.

In 2002, Huaxia Bank and China Merchants Banks became the second batch to be approved for custody licences. By the end of 2010, there were 18 custodian banks and the total AUC of the industry had reached almost 9.5 trillion RMB.

The last decade saw explosive growth of the industry. Total AUC grew a further 12-fold between 2011 and 2020, at an annual compound rate of 31.7%, according to a report published this September by China Banking Association (CBA), a unit of China Banking and Insurance Regulatory Commission.

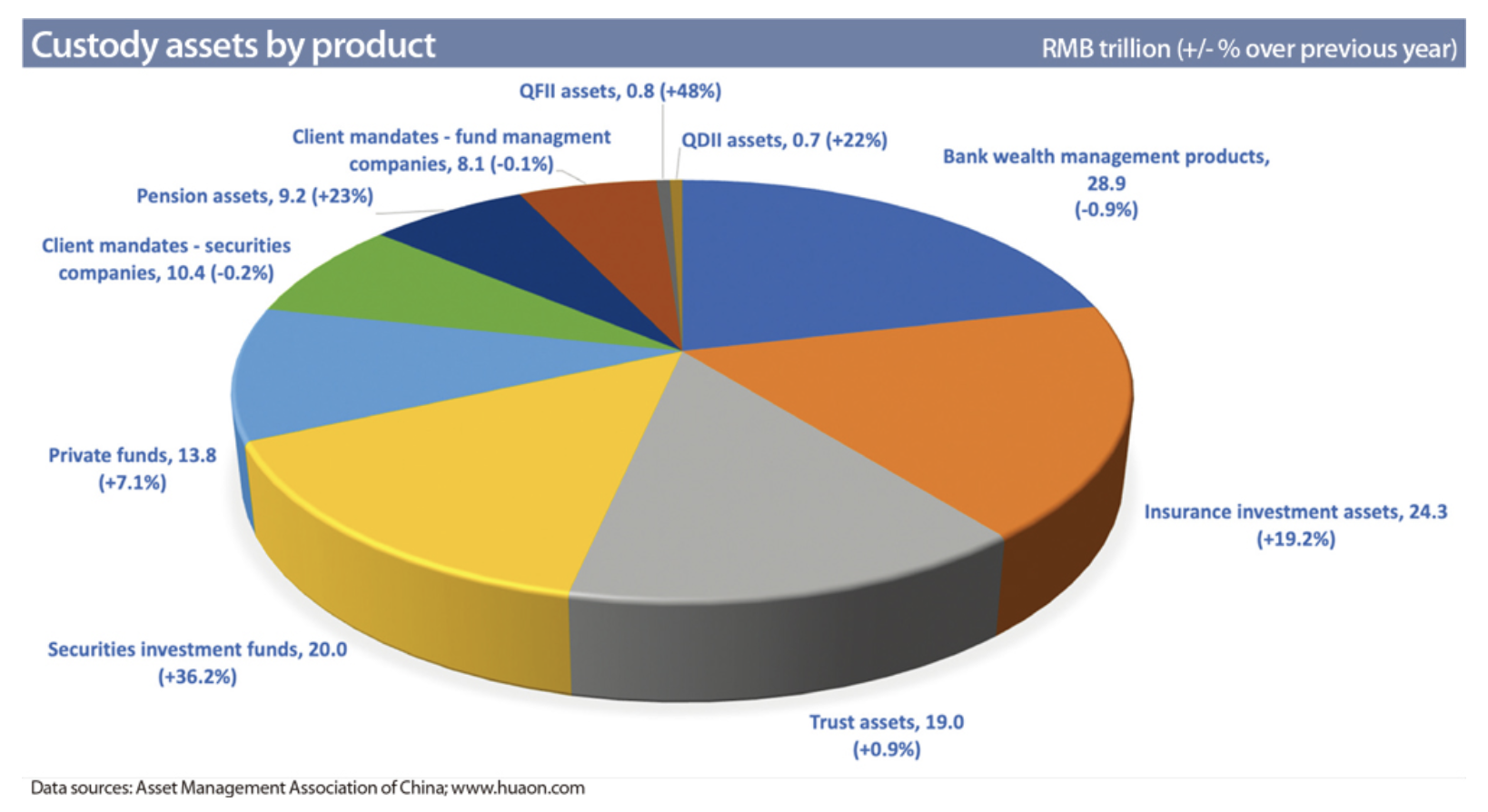

At the end of 2020, the custody industry’s total AUC topped 169 trillion RMB, up more than 10% from 2019.

The underlying products of custody assets were very diversified, reflecting the depth of the investment market. Bank wealth management products had the largest AUC, followed by insurance assets and securities investment funds.

According to the CBA report, custody revenue grew at a slower pace than custody assets in 2020, reflecting the on-going fee compression. Total custody revenue in 2020 was 52.96 billion RMB compared with 48.7 billion RMB in 2019. This means revenue rose only 8.7%, even though custody assets grew more than 10%.

Mutual funds, which had a bumper year in 2020, accounted for 30% of the custody industry’s revenues, the biggest share, and up from 6.5% in 2019. These funds received an average 9.1 basis points per dollar in custody fee, the second highest after Qualified Domestic Institutional Investor (QDII) funds, which fetched an average 9.7 basis points.

Wealth management products and trust products ranked second and third in revenue contributions at 17.5% and 11.2%, respectively.

Market share drops

China’s custody industry is top heavy, just like the global custody landscape. The ten largest custodian banks collectively accounted for over 77% of the industry’s total AUC in 2020.

But the league table may come as a surprise to those who assumed the Big Five took all the top spots, given their early start in the business. In reality, several latecomers are catching up fast. Back in 2011, the Big Five accounted for 77.3% of the industry’s total AUC. Since then, their collective market share dropped every year and was just 37.3% in 2020, less than half the share of nine years earlier.

ICBC has been the largest custodian bank since the industry’s inception but its market share slipped from 25% in 2011 to 10.7% in 2020. The bank’s custody revenue rose 7.8% year-on-year to more than 7.5 billion RMB in 2020, even though its AUC was up 18.8%, indicating strong fee compression.

China Merchant Bank, which started its custody business later than the Big Five, is now the second largest custodian bank. Its market share jumped from 2.6% in 2011 to 9.5% in 2020. Its AUC was up 21.3% from 2019, the highest growth rate among the top ten custodians. In particular, the bank won more custody assets from newly launched mutual funds than any provider in 2019, 2020, and the first three quarters of 2021.

The bank’s custody revenue was up 16.9% year-on-year to 4.2 billion RMB in 2020. But at an average of 2.6 basis points per dollar, there’s a significant gap between its revenue ratio and ICBC’s 3.8 basis points.

Collectively, the Big Five were still leading in custody assets for securities investment funds, insurance, pensions, and Qualified Foreign Institutional Investor (QFII) and QDII funds in 2020.

Securities firms enter the fray

Apart from competition from within, custodian banks are also seeing their market share being eroded by securities companies in the mutual fund and private fund sectors.

Banks were the only financial institutions qualified for custody licence until 2013, when their monopoly came to an end after 15 years. China Securities Regulatory Commission (CSRC) decided to extend qualification for custody licences to non-bank financial institutions, and Haitong Securities became the first securities house granted a custody licence that year. Since then, the number of securities houses joining the industry has mushroomed.

According to data from CSRC, 26 securities companies and 29 banks have been granted domestic fund custody licences as of September 2021.

Initially, securities companies found it very difficult to compete with banks, which can leverage their enormous distribution capabilities to secure custody appointments for mutual funds. Most securities companies’ custody mandates were won by heavy slashing of fees. According to Chinese data provider Wind Information, of the 5,227 new mutual funds set up between 2014 and 2019, only 150 selected securities companies as their custodian.

The explosive growth of exchange-traded funds in China over the past two years has allowed securities companies to find a niche by combining sales, trading, market-making, securities financing, settlement and custody as a one-stop solution for these funds. As of September, total assets of ETF funds topped 1.3 trillion RMB, according to figures from CITIC Securities. Around 16% of them are under custody by securities companies.

The introduction of the broker-clearing model for mutual funds turned the tides further. Under the traditional custodian-clearing model, mutual funds send their trade orders directly to the stock exchange, and custodian banks are responsible for clearing the trades as well as custody of the assets.

In 2019, China Clearing Corporation adopted the broker-clearing model as an alternative after a two-year pilot. This means mutual funds send their orders to their brokers, which will be responsible for verifying trades, ensuring sufficient funds and identifying irregularities before sending the orders to the stock exchange for clearing. Thus, brokers not only carry out the clearing process but also undertake the related responsibilities.

The CSRC aims to use this alternative model to mitigate clearing and settlement risk by making the broker, which is directly involved in the trade with the mutual fund, responsible for managing the risks instead of the custodian, which is not a direct party in the trade.

Securities companies now have a strong incentive to grow the assets of mutual funds to generate an on-going income stream from clearing, rather than churning funds for one-time sales commissions. This aligns their interests with that of mutual fund companies. They offer mutual funds sales, research, trading, settlement and custody as a one-stop shop.

Custodian banks have hitherto had the upper hand in the relationship with fund managers because of their enormous distribution networks and a lack of viable options in the market. They charged high fees and dictated what products they would sell. But with securities companies, as well as online mutual fund sales platforms becoming viable options, fund managers are now less at the mercy of custodian banks, and therefore are in an improved position in their working relationship.

In 2021, 1,381 new mutual funds totalling 2.34 trillion RMB were launched as of mid-October, and 86 of them used the broker-clearing model, raising more than 120 billion RMB, according to Wind Information. By contrast, only 58 funds used this model in 2020, 47 in 2019, and 14 in 2018.

Chinese business media also reported that several existing mutual funds have changed their custodian arrangements by moving assets from custodian banks to securities companies for the broker-clearing model.

Meanwhile, the rise of digital funds distribution platforms such as Tiantian Funds, Howbuy, Zhonglu and Ant Financial in recent years has eroded banks’ competitive advantage in fund distribution. Tiantian Funds, the most popular of the platforms, recorded gross sales of 1.30 trillion RMB in 2020, almost double ICBC’s fund sales. Until two years ago, ICBC was the largest fund distributor in China.

Still, securities companies are unlikely to overtake custodian banks in the near term because their total mutual fund assets under custody as of end-2020 of over half trillion RMB represented only 1.5% of the market. However, they are clearly on an upward trajectory.

Private funds

In the private fund sector, on the other hand, securities companies have won the battle resoundingly.

At the end of 2020, total assets of private funds reached almost 16 trillion RMB, with 81% under custody by a third party, according to the Asset Management Association of China. Of the funds using a custodian, 70% used securities companies.

China Merchant Securities was the largest player for private fund custody among securities companies, with over 24% market share. Guotai Junan Securities and CITIC Securities ranked second and third, with 16% and 10% market share, respectively.

Outsourcing is a critical offering for securities companies to build ‘sticky’ partnerships with private funds. In addition to custody and trading, they can provide many services, including shareholder registry, fund sales and redemption processing, net asset value calculation, performance reporting, regulatory reporting, fund information disclosure, product design advisory and online investor service platforms.

Outsourcing is highly popular with private fund companies, which are typically not very large and do not necessarily have the resources to set up their own operations. Several foreign private fund companies established as wholly-owned units of foreign firms have also been using outsourcing services from securities companies.

China Merchant Securities was the largest outsourcing provider in 2020, servicing 26,300 funds totalling 2.87 trillion RMB in assets. Guotai Junan Securities was second, servicing 11,908 funds totalling 1.85 trillion RMB in assets.

Foreign competitors

Foreign banks are also entering the scene. Seven foreign banks currently hold QFII custody licences. BNP Paribas is the latest entrant. QFII assets jumped 48% year-on-year to 800 billion RMB in 2020, and will continue to grow at a fast pace. Foreign custodians currently have around 65% share of these assets.

In addition, three foreign lenders – Standard Chartered Bank, Citibank, and Deutsche Bank – have been approved for domestic fund custody licences. However, they will take time to make an impact.

After more than two decades of growth, China’s asset management industry is now moving towards specialisation and fiduciary advisory to address a rising level of sophistication. Each client segment is developing its own specific needs, and this will require increasingly specialised expertise from both asset managers and custodians, creating room for new competitors to enter the market.

*This article was published in the Asia Asset Management’s January 2022 magazine titled “Competition stiffens”.